By Marshall J. Vest

EBR and Forecasting Project Director

September 1, 2012

The U.S. (and Arizona) economies are locked into a slow recovery that is expected to continue into next year before faster growth materializes. On the bright side, evidence continues to build that housing is beginning to heal. The biggest challenge for analysts is to get a handle on absorption of the large supply of vacant homes. Over a 30-year horizon we continue to expect Arizona to become one of the ten most populous states with over 10 million people.

The Arizona economy continues to expand at a painfully-slow pace. Key themes that we are monitoring during this growth-challenged recovery include lethargic job growth, high unemployment, miniscule income gains, cautious spending on the part of consumers, depressed migration flows, and high inventories of vacant housing.

Job growth statewide slowed significantly during the second quarter as the number of nonfarm jobs flattened (0.0%-0.5%, after adjusting for seasonality). That’s much slower than during the first quarter, when jobs were growing by 2.5% – 3.5% at a seasonally adjusted annual rate. Gains in private sector employment during the second quarter (up 2.5%-3.0% at an annual rate) were offset by losses in the public sector (declines of 3-4%). Year-on-year, job counts stood 2.4% higher in June. We look for a gain of less than 2% for the entire calendar year and only a slightly faster pace in 2013.

Initial claims for unemployment insurance are declining at a 6% annual rate in recent months and were down 15.7% Y/Y during June. Though an improvement, they are still painfully high. In June, the unemployment rate stood at a seasonally-adjusted 8.2%, the same reading for the third month in a row. We expect little improvement through the end of 2013, and unemployment not dropping below 7% until the second half of 2015.

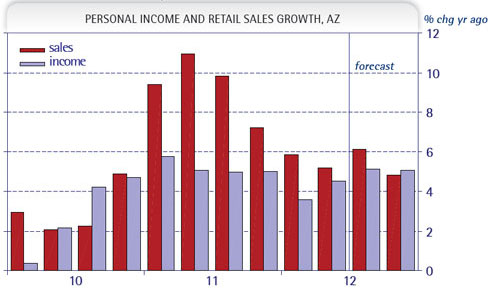

Exhibit 1: Sales Are Restrained by Incomes

Personal income statewide grew by a modest 5.1% last year but slowed to only a 3.8% gain during the first quarter. Meanwhile, a measure of retail sales that includes, retail, restaurant and bars, gasoline and food, rose by 9.3% in 2011 but slowed to an estimated 5.2% in the second quarter. So, last year’s release of pent up demand now appears to be in the rear view mirror, and spending will need support from incomes going forward. We look for personal income to grow by 4.5% this year and next before the pace quickens. Aggregate sales are expected to register gains in the 5.0%-5.5% range (Exhibit 1).

Recent housing reports have been encouraging and suggest that the healing process has begun. Home prices have been moving higher, foreclosures are down sharply, and the inventory of unsold homes has dropped dramatically. But half of would-be traditional home-buyers can’t qualify for a mortgage even with rates at record lows, mortgage delinquencies remain high, and a large portion of recent demand is from investors and new real-estate investment funds that are acquiring properties. Progress is being made, but housing markets are anything but normal.

The fall in housing prices that led to negative equity positions for many homeowners ushered in an era of reduced population mobility not seen in the U.S. for several decades. Although housing prices appear to have finally stopped falling (and are bouncing back at double-digit rates of increase, according to some measures), mobility remains depressed.

As a result, the homebuilding industry will remain subdued over the next couple of years. Although the number of residential building permits may post double-digit annual increases going forward, it will be mid-decade or beyond before building activity approaches what might be considered normal.

Long-Term Outlook

Hangover from the Great Recession continues to throttle growth, but Arizona will eventually rank amongst the fastest-growing states once again. In the annual update of our 30-year projections, we show Arizona’s population topping 10.2 million in the year 2042. That will easily put Arizona among the top-ten ranked states for the most residents. By 2042, nearly four million more people than live here today will call Arizona home. Projections for each 10-year interval for selected aggregate measures are presented in Exhibit 2.

Exhibit 2: Projections to 2042, Arizona

Highlights of the 30-year forecast include the following:

- Over 1.8 million new jobs will be created in Arizona over the next three decades, boosting the total to almost 4.3 million.

- After adding nearly 1-1/4 million persons during the decade of the “aughts,” the decade of the “teens” will see population swell by just over a million. The smaller increase is due to reduced mobility at the beginning of the decade, which is still depressing migration flows.

- Per capita personal income relative to the nation has remained relatively steady over the past 20 years at today’s roughly 87%. This ratio peaked at 95% in 1971 and was as high as 94.3% in 1986 before plunging to only 85.5% in 1992. We forecast modest improvement in the near term and a year 2042 reading of 88% — little changed from today. Per capita income is an aggregate measure whose movement depends on demographics (age structure), wage levels, industry mix, and labor force participation rates.

- Arizona’s employment-to-population ratio plunged during the current recession and will remain well below its peak established in 2000 (43.3%), and after dipping below 37.2% in 2010, finishes in 2042 at 41.9%. Arizona’s ratio consistently has consistently run 3-4 points lower than nationwide. This ratio is a full five points lower in metro Tucson than in metro Phoenix.

- As the population continues to age, an increasing share of personal income will come from transfer payments, of which social security is the largest component. The share will rise from 20.3% today to 26.2% by 2042. Per capita transfers in Arizona jumped during the Great Recession and will continue to run higher than the corresponding nationwide measure.

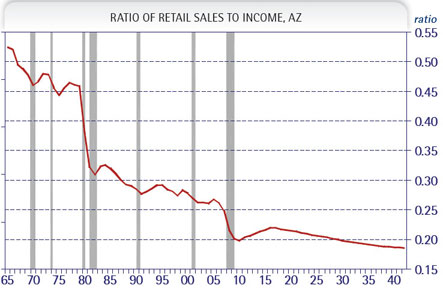

Exhibit 3: Retail Sales Relative to Income Has Fallen Significantly

- Retail sales relative to income fell significantly during the Great Recession, dropping below 20% from nearly 53% in the mid-1960s. An aging population that spends more on services (especially health care) and a smaller portion on taxable goods, along with a narrowing of the tax base, accounts for the drop. This ratio will sink to an all-time low of 18.6% in another 30 years. This has serious implications for a tax system heavily reliant on retail sales (Exhibit 3).

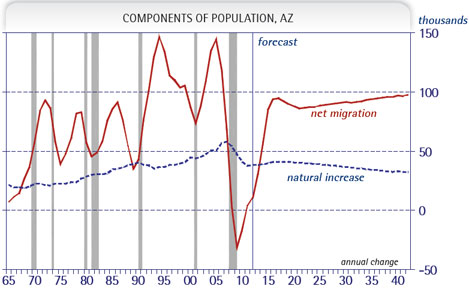

- Over the long term, migration flows will continue to account for the lion’s share of population growth. On average, natural increase (births minus deaths) accounts for one third while net migration provides the remainder. The latter varies significantly, of course, over the business cycle. During the recession, with mobility rates at a six-decade low, migration flows swung deeply negative for the first time in recorded history. By 2016 net migration will again approach 95,000 annually. Natural increase moved significantly lower during the recession due to falling births, but will stabilize at 40,000 new residents annually in the near term, before moving lower as the population ages (Exhibit 4).

Exhibit 4: Population Flows are (Very) Cyclical

- Government, manufacturing, leisure & hospitality, utilities, mining, and utilities will represent smaller shares of total jobs 30 years from now. Government’s share will decline from 16.7% to 13.6%, manufacturing from 6.2% to 4.2%, leisure & hospitality from 10.9% to 10.3%, and utilities from 0.5% to 0.3%. Mining jobs will all but disappear, accounting for two-tenths of one percent and only 7,400 jobs in 2042.

- Sectors that will gain the largest shares are professional and business services (from 14.4% to 16.8%), health care & social assistance (from 14.9% to 18.2%), and financial services (from 6.9% to 7.4%).

- Retail trade (12.2%), construction (4.7%), other services (3.6%), transportation and warehousing (2.9%), and information (1.5%) share remain largely unchanged.

- In our “high” scenario, Arizona’s population reaches 11.2 million in 2042. In the “low” scenario, it is 9.8 million, compared to 10.2 million in the “most likely – or Base” scenario. Michigan, the seventh largest state, today has 9.9 million.

- Today, Arizona’s 6.4 million population ranks 16th, just ahead of Tennessee. In thirty years, Arizona likely will overtake Indiana, Massachusetts, Washington, Virginia, New Jersey, North Carolina, and Michigan to become the ninth largest state.

- The range for 2042 metro Phoenix population is 6.9 to 7.5 million. Metro Tucson’s range is 1.3 to 1.5 million people. The “Sun Corridor” megapolitan population (both metros — three counties combined) ranges from 8.2 to 9.0 million.

- By 2042, 70% of Arizona’s population will reside in the Phoenix metro area (Maricopa and Pinal counties). Metro Tucson (Pima County) will account for 14.0%. Today, the shares are 65.8% and 15.3%, respectively.

Arizona was the second-fastest growing state over the past decade, even though population growth disappeared during the recession. Low mobility rates will limit Arizona’s growth for a few more years, but growth will return to more historical levels by mid-decade.

Over the next 30 years, Arizona will add 3.7 million residents or a little more than half of the numbers here today. 3.1 million will land in metro Phoenix. We can only guess what Arizona will be like, but it’s clear that a great deal of change lies ahead.

Arizona Horizon image courtesy Shutterstock.

Leave a Comment