By Alberta H. Charney, Ph.D.

Senior Research Economist

November 1, 2013

Introduction

Priorities, attitudes, politics and available public funding all influence both the level of state spending and the mix of those expenditures. This article provides a historical view of Arizona’s expenditures by major spending category. Long-term trends in both the mix of spending and the level of spending, adjusted for population and inflation, will be presented.

Money spent by the state of Arizona can be categorized roughly into three types: appropriated general fund money (mostly taxes), non-general fund appropriated money, and non-appropriated funds. The focus of this article is the trend and mix of general fund appropriations, though it is difficult and somewhat meaningless to discuss only general fund money without reference to state expenditures from other sources.

Contents:

- Definitions

- Total General Fund Expenditures

- Expenditure Mix of the General Fund

- Conclusion

- Footnotes

Definitions

Appropriated general fund money is derived primarily from the state’s income and sales taxes and deposited into the general fund. Portions of both the state income and sales tax are distributed to cities and/or counties, so the general fund includes only those revenues made after those distributions are made. The legislature has the most control over general fund money and this category is the focus of this article. It is important to understand, however, that this is only a portion of total money expended by state agencies.

Appropriated non-general fund money can come from a variety of sources and, although it does not pass through the general fund, it is still subject to the appropriation process. This is money that can be spent only in certain ways, but is still “appropriated.” Two major examples of this non-general fund, or “other” appropriated, money are transportation funds and tuition at higher education institutions. Although tuition is paid directly by students and their families, rather than being derived from a general tax, and is not part of the general fund, a portion of it still falls under the appropriations process. All highway-related taxes and fees are “earmarked” for spending on transportation. That is, the highway taxes and fees (e.g., gasoline tax, use fuel taxes which are primarily paid on diesel fuel, license fees, weight fees) cannot be spent for any other purpose, as outlined in the Arizona State Constitution. These dollars are collected, portions are shared with cities and/or counties for transportation purposes and the rest is spent by the state on road construction and maintenance. Although this money must be spent on roads, it still involved the appropriation process. Of course, federal transportation dollars, given to the state for the purpose of maintaining the federal highway system in the state, are typically considered non-appropriated funds.

Non-appropriated funds are derived mainly from non-state sources. Examples of non-appropriated funds are federal dollars that come into the state to fund a wide variety of programs. For example, federal dollars that pay healthcare costs for low-income individuals via the Arizona Health Cost Containment System, or AHCCCS (Arizona’s version of Medicaid) enter and are expended from state coffers, but the money’s intended use is pre-determined and it is not included in the legislative appropriation process. The legislative process is not independent of the amount of money that is received from the federal government for this purpose, however, because there is a required match for each major category of healthcare funds (e.g., for every federal dollar that is spent on Arizona health care, the state must also contribute a certain amount, sometimes 10% or less). Other examples of non-appropriated funds are grants and contract dollars received by universities. This money is required to be spent on the research/project that is being funded by those dollars and to pay the associated university overhead costs (e.g., administration, ongoing research lab costs), so this money falls outside of the appropriations process.

There are other state expenditures that don’t fit into any of these three categories. An important one is the State Retirement System. Although funded by a combination of general taxes (state employee-related expenses) and employee contributions (deductions from wages), it is a pot of money designated to provide payouts to retirees and is, therefore, completely outside the appropriations process.

In addition to state-related money that funds the major state functions that will be discussed below, local governments also either help to pay for some of the services provided or they directly provide similar services at the state level. More about this will be said within the discussions of each major spending category.

The rest of this article focuses on the level and mix of the expenditures from the general fund of the state of Arizona. The legislature has the most control over this money and therefore the level and mix of the general fund revenues reflects both the priorities of the legislature and the realities of the ongoing economic conditions.

back to topTotal General Fund Expenditures

Six major expenditure categories were tracked over time i. Three of them fall under the broad category of Health and Welfare: AHCCCS (Arizona’s version of Medicaid), the Department of Health, and the Department of Economic Security. Two of the remaining three categories are for education: K-12 Education (combined spending of the Department of Education and spending on Charter Schools and School Facilities) and Higher Education (the combined expenditures for Community Colleges and the University System). The sixth category is for Corrections, which includes spending on both adult and juvenile correction. The Other category represents the residual between total general fund expenditures and the six categories just listed.

Total general fund expenditures have increased over the 31-year period from FY1982 through FY2012 by an annual average compound rate of 5.9 percent. While that seems high, it must be remembered that Arizona’s population grew by an annual compound rate of 2.7 percent over the same period and the cost of living (as measured by the Consumer Price Index for the Western Region) increased by 2.9 percent, compounded per annum. Therefore, total general fund expenditures may or may not have kept up with population growth the cost of providing government services.

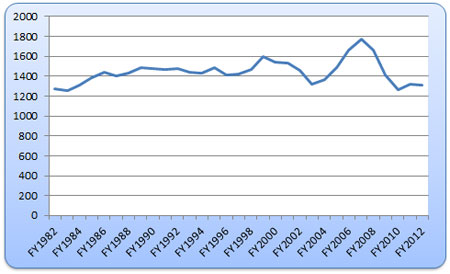

Figure 1: Arizona Deflated ($2012) Per Capita General Fund Expenditures 1979-2012*

*1979-2011 are actual expenditures; 2012 is appropriations

Figure 1 shows total general fund expenditures, divided by Arizona population, and adjusted for inflation by dividing by the CPI for the Western Region (adjusted so that the base is equal to 1 in 2012). The resulting graph depicts per capita deflated general fund expenditures in 2012 dollars. Per capita deflated expenditures were $1,277 in FY1982. At this time, the economy was just exiting the recession that occurred between August 1981 and November 1982. Deflated per capita expenditures were rather constant between FY1985 and FY1997, $1,441 in $2012.

There was a small increase in FY1998 and FY1999 and a decline from FY2000 through FY2002. The decline was likely due to the recession that began and ended in 2001. The substantial increase in deflated per capita expenditures from FY2003 through FY2006 reflects the overall growth in the economy, which was driven by construction and what is now recognized as the housing bubble. The housing crises and recession that began in late 2007 reduced per capita government expenditures from a high of $1,768 ($2012) in FY2007 to a low of $1,260 in FY2010. Since then, there has been a small increase to $1,314 in FY2012. Per capita deflated expenditures from the general fund in FY2012 were $37 more than they were in FY1982.

FY2012 expenditures were approximately $133 per person below the 1982-2011 average of the deflated per capita expenditures of $1,447, or 9% below the historical average. The range of deflated per capita expenditures around the FY1982-FY2011 average was from $188 below average in FY1983 to $321 above average in FY2007.

back to topExpenditure Mix of the General Fund

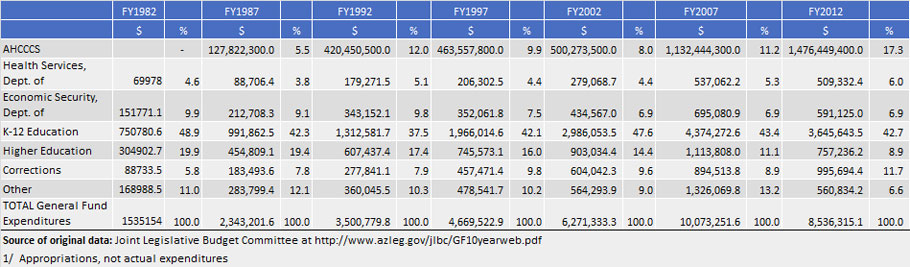

The mix of expenditures from the general fund has changed dramatically over time. Table 1 gives expenditures from the general fund, disaggregated into the six categories described above, at five-year intervals from FY1982 through FY2012 and the percent distribution. The largest change has been the spending on the Arizona Health Cost Containment System (AHCCCS) from 0% of the general fund in FY1982 to 17.3% in FY2012. Prior to the creation of AHCCCS, all indigent health care was provided by counties in Arizona. In 1965, the US Congress passed Medicaid and by 1972, all states were receiving federal Medicaid funds except Arizona. The counties appealed to the Arizona Legislature for relief from the health care burden and the legislature established AHCCCS. Medicaid is funded as a fee-for-service while AHCCCS set up a system to pay health care providers on a per patient basis. AHCCCS began as a demonstration project for the Medicaid system and has become a model project for providing quality health care at a low cost. By qualifying as an approved alternative to Medicaid, the state was eligible to receive federal money for healthcare ii.

Arizona Health Care Cost Containment Services

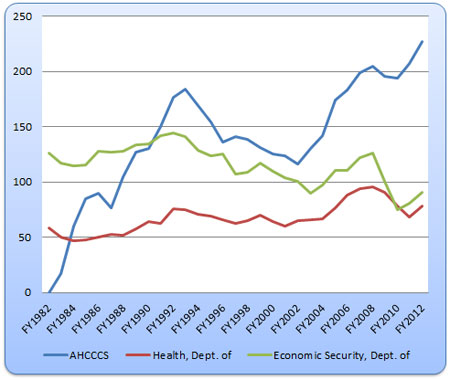

The share of total general fund expenditures devoted to healthcare has increased for several reasons. Since the goal of AHCCCS was to both improve healthcare for low-income individuals and to reduce the healthcare burden of the counties, additional state expenditures were obviously required. Over time, the per capita income of Arizonans has declined relative to the rest of the nation over the 31-year time period, with the result that a larger share of Arizona residents have become eligible to participate in the program. Recessions strongly affect AHCCCS rolls. When the economy weakens and suffers job losses, people lose their employer-based health care, incomes fall and more individuals and families become eligible for participation in AHCCCS. Over time, the scope of services provided by AHCCCS has also expanded, such as the addition of long-term care and mental and behavioral health coverage. In addition, changes in the income requirements (income relative to the U.S. poverty level) have resulted in more Arizonans becoming eligible for AHCCCS programs. Deflated per capita expenditures on AHCCCS climbed steeply after the program began to $184 in FY1993, declined to a low of $116 in FY2002 and his continued to climb to $227 in FY2012 (Figure 2). Because AHCCCS is an approved Medicaid program, substantial federal dollars support the state’s health care program. Total AHCCCS spending from all sources, as reported in the State of Arizona Appropriations Report for 2012 (AR2012) iii, was just under $6 billion dollars. Of that, less than 23 percent was to be paid from the general fund. The Federal Medicaid Authority paid approximately 66 percent of the total and a variety of other sources, including county funds and the tobacco litigation settlement fund, accounted for the small remainder.

back to topArizona Department of Health Services

The portion of general fund expenditures devoted to another health-related state expenditure category, the ADHS, has also grown slightly from 4.6% to 6% of total general fund expenditures (Table 1). According to the ADHS website, they operate a wide variety of programs that includes disease prevention and control, health promotion, community public health, environmental health, behavioral health, maternal and child health, emergency preparedness and regulation of childcare and assisted living centers, nursing homes, hospitals, other health care providers and emergency services iv. In deflated per capita terms, expenditures by the ADHS have also increased slightly, from approximately $50 during the FY1984-FY1986 period to $68 – $78 in recent years. Substantial federal funds also contribute to the services provided by the ADHS, with the result that the amounts shown in Table 1 represent only 28% of the almost $1.8 billion expenditures made by this agency (AR2012).

Table1: Total General Fund Expenditures ($Thousands and % Share)

Arizona Department of Economic Security

Also within the Health and Welfare category of services is the ADES. ADES provides a wide variety of services and administers a substantial amount of federal funds that support many of their functions. Their programs

Figure 2: Arizona Deflated ($2012) Per Capita General Fund Expenditures for Major Programs

*1979-2011 are actual expenditures; 2012 is appropriations

are numerous and include those for the aging, the homeless, domestic violence, children and youth support services, foster care placement, adoption services, programs for the developmentally disabled and work-related programs such as day care subsidies, rehabilitative services and unemployment insurance. ADES expenditures fell as a share of total general fund expenditures from 9.9 percent in FY1982 to 6.9 percent in FY2012. In addition to ADES’ share of general fund expenditures declining, deflated per capita expenditures also fell from approximately $144 per person if FY1992 down to between $75 to $91 in recent years (Figure 2). Substantial amounts of federal dollars support many of the programs provided by ADES. The total amount of spending by ADES from all sources was over $2.7 billion dollars (AR2012). Of this, only 22 percent would be paid for from the general fund. The remainder was mostly federal dollars, although some smaller funds also contributed to total expenditures.

K-12 Education Spending

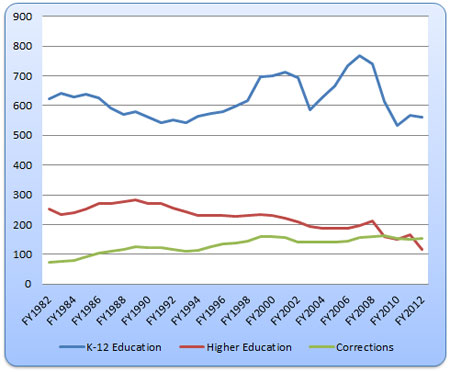

The largest portion of state general fund expenditures is for K-12 spending. Most of this is through the Arizona Department of Education (ADE), although state funds for Charter Schools and for school facilities were included in this series to maintain a consistent K-12 spending category. As a share of total general fund expenditures, K-12 spending ranged from 37.5 percent in the early 1990s, which was substantially down from the share high of 48.9 percent in FY1982 (Table 1). On a deflated per capita basis, spending fell from $624 in FY1982 to a low in the FY1990-FY1993 time period of approximately $550 (Figure 3). After FY1997, K-12 expenditures became extremely volatile, increasing to $712 then falling back to $585 as a result of the 2001 recession. This was followed by another rapid growth period associated with the construction-driven expansion to reach a peak of $768 in FY2007 and crashing to the lowest level of the entire period in FY2010 ($533). The level of per capita deflated K-12 spending has increased slightly since then.

Although there are some federal dollars flowing into Arizona for K-12 expenditures, almost 70 percent of the total state expenditures from all sources is derived from the state general fund (computed from AR2012).

It is important to note that the total spending by ADE of $4.9 billion shown in the AR2012 does not represent total spending in the state on K-12. It only represents the portion spent by the state. Each school district raises additional funds locally through local property taxes. Comparing total state and local expenditures on Elementary and Secondary School in FY2011 from the Census Bureau’s State and Local Government Finance 2010-2011 (SLGF2011) v to the agency total in the State of Arizona Appropriations Report for 2011 (AR2011), suggests that local property taxes contribute an additional amount equal to approximately 60% of the figure reported in AR2011 vi. So, out of the total amount of K-12 money shown in the appropriations report, $0.70 of every $1 in K-12 education is paid for out of the general fund. In addition, another $0.60 is collected via property taxes by local governments (school districts) and spent on K-12 education. Theses figures should be viewed as very rough approximations because a) the data reported in the Census Bureau publications are not perfectly consistent with state publications due to differences in definitions, b) the figures used in this article for 2012 are based on appropriations, not actual spending, and c) the figures in appropriations books differ from final appropriations because of revisions.

back to topHigher Education

Figure 3: Arizona Deflated ($2012) Per Capita General Fund Expenditures for Major Programs

*1979-2011 are actual expenditures; 2012 is appropriations

This category includes spending on both Universities and Community Colleges. The share of general fund spending on higher education has fallen from almost 20 percent in FY1982 to less than 9 percent in FY2012 (Table 1). Deflated per capita expenditures in this category averaged approximately $275 annually during the FY1986-FY1991 period, which was the highest level in the 31-year period shown. Since then, there has been a steady decline, reaching $116 in FY2012. Deflated per capita higher education spending has declined by almost 60 percent since the FY1986-FY1991 period (Figure 3). Community colleges, like K-12 school districts, can impose property taxes to cover some of the reductions from state government. Of course, like all local governments, community colleges are limited in how much additional funds they can raise because of strict state-imposed levy limits. In addition, community colleges receive tuition payments and fees from students.

Universities have no local taxing authority. To cover reductions in expenditures from the general fund, they raise tuition paid by students to attend. In 1982, the total “appropriated receipts,” i.e., tuition, were approximately 23 percent of total appropriated funds, which included both general fund and tuition (State of Arizona Appropriations Report for 1982). In FY2012 tuition and fees (collections fund) was almost 54 percent of total appropriated funds (computed from AR2012). Therefore, over the last 30 years, the share of total university appropriated funds (tuition, fees and general fund money) paid by students in the form of tuition and fees has more than doubled. But this comparison underestimates the total tuition and fees paid currently by students and their families because not all tuition and fees are allocated to the Collections Fund so they are not appropriated. Rather, substantial portion of tuition and fees are deposited into local funds of the universities. The Collections Fund figures used in these calculations was approximately 60% of the total tuition and fees collected in FY2012, computed by comparing AR2012 with the Arizona Board of Regent’s Annual Research Report for 2012 (ABOR2012) vii.

Universities have substantial other money flowing through (as shown in AR2012). The general fund contributes approximately 17 percent of the total amount of money that passes through the universities. Tuition, part of which is appropriated and part of which is not, forms a significant portion, more than $1 billion. In addition, there is more than a billion dollars in research-related money (including indirect costs) brought into the state (ABOR2012). Most of that money is restricted because it must be used to conduct the research agreed to in the research contracts. The rest of the non-appropriated funds are mainly auxiliary funds that are associated with enterprise activities on campuses, e.g., book stores and food sales.

back to topCorrections

Corrections expenditure (adult and juvenile) is the last of the six largest categories of spending from the general fund. Corrections expenditures grew almost twice as fast as the overall general fund so it’s share increased from 5.8% in 1982 to 11.7% in 2012. Deflated per capita corrections expenditures more than doubled from $74 in FY1982 to $153 in FY2012 (Figure 3). Unlike AHCCCS and the Department of Health Services, which receives substantial federal dollars to help provide services, 89 percent of all state correction spending is from the general fund. Of course, the state pays only for state correction facilities. There are also correctional facilities owned and operated by local governments throughout Arizona. In SLGF2011, state spending on corrections was $856.6 million and local government spending was $598.5 million (total $1,646.2 million).

back to topConclusion

This article provides an overview of the level and mix of general fund expenditures over a 31-year period. Total expenditures from the general fund have been volatile at times, reflecting the booms and busts of the Arizona economy, particularly over the last 15 years. In FY2012, deflated per capita expenditures from the general fund were similar to what they were during the 1981/82 recession. The volatility of total deflated per capita general fund expenditures most closely resembles the ups and downs in K-12 expenditures. The amount of volatility shown in K-12 expenditures creates uncertainty and continuity issues, making it more difficult for K-12 administrators to plan and utilize resources effectively. As the largest spending category, K-12 Education is all too often the one that is affected the most when downturns occur. The two healthcare categories, AHCCCS and the Department of Health, have substantially grown over this period, both as a share of the total general fund and as deflated per capita expenditures. Much of this growth is necessitated by need as employer-provided health insurance has declined and Arizona’s per capita income has not grown as fast as it has in the rest of the nation. In addition, the scope of Arizona’s AHCCCS services has expanded over the years and changes in eligibility have allowed additional families to qualify. The two categories showing the least volatility are expenditures on higher education and corrections. Higher education expenditures, on a per capita deflated basis, have shown a steady decline over most of the 30-year period and expenditures on corrections has shown a steady increase. In FY2012, the state spent more out of the general fund on incarcerating people than it did on the higher education system.

back to topFootnotes:

i. All expenditure data were obtained from the Joint Legislative Budget Committee’s website: http://www.azleg.gov/jlbc/GF10yearweb.pdf, accessed August 2013.

ii. A somewhat longer history of AHCCCS is available: http://www.azahcccs.gov/Careers/History.aspx, accessed August 2013.

iii. http://www.azleg.gov/jlbc/12app/FY2012AppropRpt.pdf, accessed August 2013

iv. http://www.azahcccs.gov/Careers/History.aspx, accessed August 2013

v. State and Local Government Finances 2010-2011 can be found at: http://www.census.gov/govs/local/

vi. The 2011 Appropriations Report is at: http://www.azleg.gov/jlbc/11app/FY2011AppropRpt.pdf

vii. Arizona Board of Regents, 2012 Annual Research Report, found at http://azregents.asu.edu/ABOR%20Reports/2012-Annual-Research-Report.pdf, accessed August 2013.

Arizona flag and credit card photo courtesy Shutterstock.