Second Quarter 2019 Forecast Update

By George W. Hammond, Director and Research Professor, EBRC

The Arizona economy continues its long winning streak. Employment is expanding, population growth is solid, and wages are rising. Further, Arizona continues to far outpace national growth rates. The only smudge on this picture is the state unemployment rate, which remains stubbornly above the U.S. average. The likely explanation for that lies in the state’s strong job growth, which is drawing more residents to the state and more discouraged workers off the sidelines and into the labor market.

The outlook for 2019 remains solid for the state and nation. The current national expansion is very much on track to be the longest on record. However, gains are expected to slow from above trend rates last year to below trend rates by 2020. This implies that recession risks are elevated beginning in 2020. Nonetheless, the most likely scenario remains continued gains in the near term, with more jobs, residents, and income in Arizona.

Arizona Recent Developments

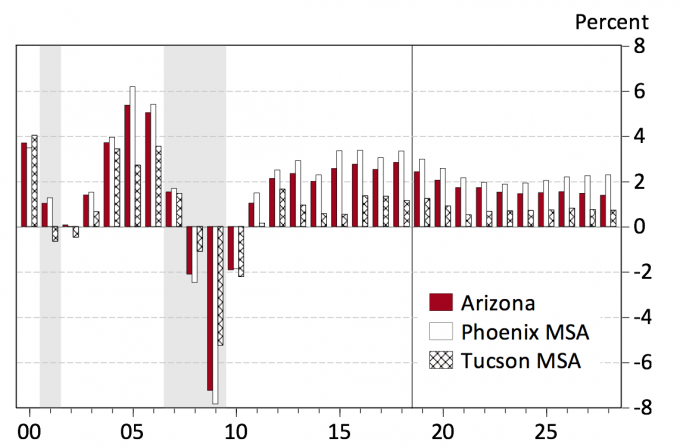

Arizona added 78,800 jobs in 2018, which translated into 2.8% growth, according to the latest revised data from the U.S. Bureau of Labor Statistics. As Exhibit 1 shows, that was up from 2.5% in 2017. Employment gains also accelerated in the Phoenix Metropolitan Statistical Area (MSA), rising from 3.0% in 2017 to 3.3% in 2018. In contrast, job growth decelerated in the Tucson MSA, from 1.3% in 2017 to 1.2% last year. Nationally, job growth was 1.6% in 2017 and 1.7% in 2018.

Overall, as the exhibit suggests, job growth last year in Arizona, Phoenix, and Tucson was similar to gains posted since 2015-2016.

Exhibit 1: Arizona Job Growth Accelerated Last Year (Annual Job Growth Rates)

While Arizona job growth picked up some steam last year, it did not translate into much improvement in the state’s unemployment rate. In 2018, the average unemployment rate was 4.8%, compared to 4.9% in 2017. Even though the rate was far below its recent peak in 2010 of 10.4%, it remained well above the national average of 3.9%. The Phoenix MSA unemployment rate was 4.2% in 2018. In the Tucson MSA, the rate was 4.5%.

Arizona’s unemployment rate has been above the national average for more than a decade. Initially, that was likely due to the fact that the state was hit much harder during the Great Recession than was the nation. However, as the recovery progressed, the gap has shown little sign of closing. What accounts for that? One possible explanation is that Arizona’s strong growth has pulled more than enough workers into the state and off the sidelines of the labor market.

Construction employment has been rising rapidly. It increased 10.6% during the past four quarters. This has been supported by increased housing permit activity. According to preliminary estimates from the U.S. Census Bureau, statewide total housing permits rose 5.5% last year, to hit 41,630. The gain was driven by a 12.0% increase in single-family permits. Multi-family permits decreased 10.5% in 2018.

Total housing permits rose 9.0% in the Phoenix MSA last year, with single-family permits up 13.6% and multi-family permits down 1.7%. Total permits declined 4.8% in the Tucson MSA last year, after very strong performance in 2017. Multi-family activity declined by 33.0% while single-family permits rose 11.0%.

Arizona house prices rose 8.9% over the year in the fourth quarter of 2018, according to the latest data from the Federal Housing Finance Agency. These data track repeat sales of single-family homes for all transactions, before adjustment for inflation. Arizona far outpaced the national rate (6.0%) during the period, but state gains slowed from 9.2% during the third quarter. By the same measure, Phoenix MSA house prices rose 9.8% in the fourth quarter, while Tucson MSA prices increased 7.6%.

In the last quarter of 2018, Phoenix MSA house prices finally regained the previous peak achieved in the fourth quarter of 2006. Statewide house prices remained 1.9% below the previous high. Tucson has more ground to make up, with prices 9.6% below the pre-recession high. Nationally, house prices were 14.3% above the previous peak. Keep in mind that inflation-adjusted house prices remain well below peak for the U.S., Arizona, Phoenix, and Tucson.

Personal income in Arizona increased 5.5% last year, according to the preliminary estimates from the U.S. Bureau of Economic Analysis. That was well above the national rate of 4.5%. Further, Arizona’s personal income ended the year strong, rising 5.9% over the year in the fourth quarter. That beat the U.S. at 4.6%.

On a per capita basis, state personal income rose 3.7%, which was just below the national increase of 3.8% in 2018. Arizona’s per capita personal income, at $43,650, was 18.7% below the national average of $53,712. That ranked the state 42nd in the nation.

Personal income includes earnings from work, asset income (dividends, interest, rent), and transfer receipts. In 2018, 3.6 percentage points of the 5.5% growth was generated by earnings from work. Asset income and transfer receipts contributed 1.0 percentage points each. The components do not sum perfectly to 5.5% due to rounding.

Arizona Outlook

While the national economy continues to post strong growth, it is expected to slow gradually through the next few years. Real GDP increased by 3.2% in the first quarter of 2019, which was a strong result. The April 2019 baseline forecast from IHS Markit calls for growth to slow to the 2.0% range in coming quarters. On an annual basis, real GDP growth is forecast to decelerate from 2.9% last year to 2.3% in 2019, 2.1% in 2020, and 1.9% in 2021.

Decelerating national growth in the near term is driven by slower global growth, the lagged impacts of past interest rate increases, diminished federal fiscal stimulus, tariffs, and approaching capacity constraints. Overall, the forecast calls for the U.S. economy to transition from above trend growth in 2018 to below trend growth by 2020. That pattern implies increased recession risks in 2020.

The outlook for monetary policy calls for the Federal Reserve to increase the target for interest rates once this year. That translates into an increase in the federal funds rate from 1.8% last year to 2.4% in 2019. Further tightening is expected in 2020, driving the rate to 2.6% where it stabilizes. The 30-year conventional mortgage rate is forecast to rise from 4.4% this year to 4.8% by 2021.

Interest rate spreads remain close to zero, but have not yet turned negative, at least in the monthly data. The spread between the 10-year and 2-year Treasury rate reached 0.1 percentage points in April and was slightly negative for a week in late March before returning to positive territory. The spread between the 10-year and 3-month Treasury rate has been more stable lately and was 0.19 percentage points in April. Overall, interest rate spreads remain a source of concern but do not yet provide a decisive recession signal.

Federal fiscal stimulus gradually fades in the near term, with real federal government spending on goods and services sliding from growth of 3.7% this year to 0.9% next year, and then declining modestly in 2021.

Inflation remains under control, with the CPI-U increasing 2.1% this year, 2.0% next year, before accelerating modestly to the 2.3% per year range by 2021.

Continued real GDP growth drives the national unemployment rate down to 3.6% this year, where it remains stable through 2020. Slowing output growth is expected lift the rate modestly in 2021 to 3.8%.

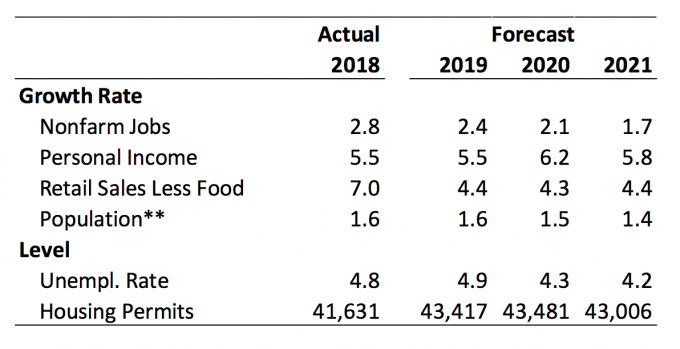

The U.S. outlook sets the stage for the Arizona forecast, because the state depends in part on national (and global) markets to drive demand. Exhibit 2 summarizes the Arizona forecast through 2021. Job gains are forecast to decelerate from 2.8% last year to 2.4% in 2019, then to 2.1% in 2020, and 1.7% in 2021. Slowing national growth drives the near term slow down.

Exhibit 2: Summary of the Arizona Outlook

Most of the job growth is concentrated in service-providing sectors, especially education and health services; professional and business services; leisure and hospitality; and trade, transportation, and utilities. These four industries alone account for 74.1% of job gains through 2021.

With rising employment comes increased income. Arizona personal income is projected to rise by 5.5% this year, then 6.2% in 2020, and 5.8% in 2021. Solid gains reflect tightening labor markets in the state, as well as continued increases in the state minimum wage through 2020.

Solid income gains translate into increasing consumer spending in the state. Retail sales gains slow from 7.0% last year, a very strong gain, to a more normal pace around 4.4% during 2019-2021.

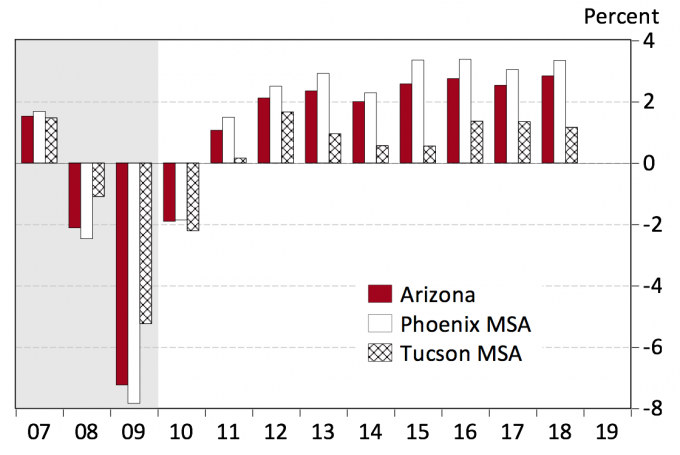

Overall, if the national economy continues to grow, Arizona is poised to generate strong gains. Within the state, the Phoenix MSA is forecast to generate the most of the growth expected for Arizona. Exhibit 3 shows that job growth is expected to decelerate during the next decade for all three geographies. This slowdown is driven by demographics, as the baby boom generation gradually ages out of their prime work years. Tucson also generates job growth under baseline assumptions, but increases come at a slower pace.

Exhibit 3: Most Arizona Job Gains Are Concentrated in Phoenix, but Tucson Contributes as Well (Annual Job Growth Rates)