Delaney O’Kray-Murphy, EBRC research economist

Valorie Rice, senior business information specialist

Prarthana Magon, EBRC student researcher

Current data releases as of 9 June 2023

Housing affordability increased nationally and in all Arizona metropolitan areas for the first quarter of 2023 based on the latest National Association of Home Builders/Wells Fargo Housing Opportunity Index (released June 8). Rising incomes and lower home prices contributed to improved affordability. New and existing homes sold nationally between January and March were affordable to 45.6% of families earning the U.S. median income. This was a larger share than in the fourth quarter of 2022 when only 38.1% of homes sold were affordable, but still far below the rate of 56.9% in the first quarter of 2022. Arizona metropolitan areas followed suit, as the share of affordable homes increased across the board at the beginning of 2023 yet fell short of the rates from a year ago. Tucson once again moved above the U.S. in the first quarter of 2023, with 46.8% of homes sold affordable to a family earning the median income, after having a smaller share of affordable homes than the nation for the last three quarters: Tucson historically has better housing affordability than the nation. The most sizable jumps in affordability were in the two areas of the state that are typically the most affordable – Sierra Vista-Douglas and Yuma – with more than 20 percentage points increase each from the last quarter of 2022 to the first quarter of 2023. The shares of homes sold affordable to families earning median income in Arizona metropolitan areas for the first quarter of 2023 were 64.6% in Sierra Vista-Douglas, 63.6% in Yuma, 46.8% in Tucson, 41.9% in Lake Havasu City-Kingman, 34.3% in Phoenix, 29.2% in Flagstaff, and 23.9% in Prescott Valley-Prescott. The least affordable housing markets were all in California.

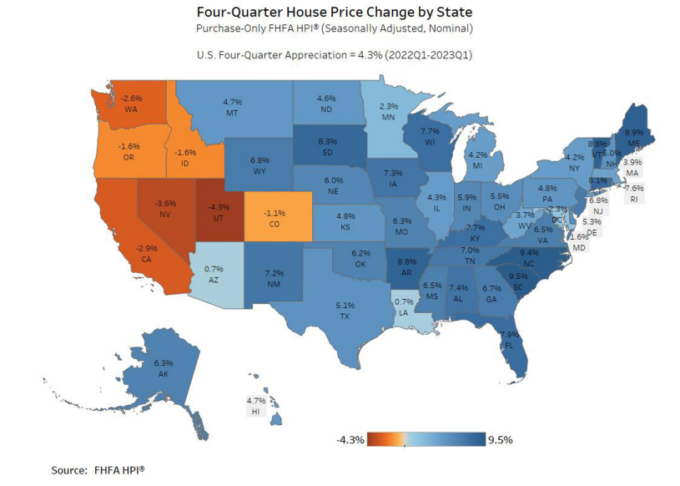

Arizona house prices barely increased between the first quarter of 2022 and the first quarter of 2023, moving up 0.7%, according to the Federal Housing Finance Agency (FHFA) House Price Index released May 30. Unlike Arizona, most western states had depreciation of house prices. South Carolina followed by North Carolina lead year-over-year house price increases in the first quarter of 2023. The South Atlantic region had the largest one-year change in house prices at 7.2%, the Mountain (-0.1%) and Pacific (-2.4%) regions had negative house price changes. Nationally, house prices gained 4.3% during the same period, seasonally adjusted. Data for the nation and states are for the purchase-only index. The House Price Index has information for all metropolitan areas for an all-transactions index that includes both purchase and refinance mortgages. The one-year changes in house prices for the Arizona metropolitan areas in the first quarter of 2023 were 4.3% in Flagstaff, 4.7% in Lake Havasu City-Kingman, 3.4% in Phoenix, 7.8% in Prescott Valley-Prescott, 5.3% in Sierra Vista-Douglas, 9.9% in Tucson, and 4.0% in Yuma.

Arizona’s non-seasonally adjusted total building permits experienced declines both month over month and year over year, according to the May 23 US Census Bureau Building Permits Survey. The total number of permits fell to 4,268, indicating a 34.6% decrease compared to the previous month and a 19.0% decrease compared to the same period last year. Among the different permit categories, two and three-to-four-unit permits showed slight increases over the month. However, permits for single family and five or more-unit buildings witnessed significant decreases. In Phoenix, a similar trend was observed, with an overall decline in permits primarily driven by a notable decrease in permits for single family and five or more-unit buildings. The growth in other areas was not sufficient to compensate for this decline. In Tucson, decreases were seen across all permit categories. The reported permit numbers for Phoenix and Tucson were 3,287 and 355, respectively. Notably, Phoenix managed to surpass its permit level from April 2022. Analyzing the different counties, Apache, Cochise, Maricopa, Mohave, Navajo, and Pinal experienced month over month decreases in permits. On the other hand, Coconino, Graham, Gila, Santa Cruz, Yavapai, and Yuma witnessed increases.

Building Permits Issued for New Private Housing Units

Phoenix housing prices were down 4.5% over the year in March. It was not alone, as half of the 20 cities contained in the S&P CoreLogic Case-Shiller Indices experienced negative house price changes over the year, most of them being in the West. Nationally, house prices gained 0.7% in March compared to 2.1% in February. The 20-city composite had a loss of 1.1% over the year according to the May 30 release. Despite decreases overall, cities in the Southeast exhibited strong price gains. Miami had the largest increase in house prices for an eighth month in a row, posting a 7.7% year-over-year increase for March followed by Tampa at 4.8% and Charlotte at 4.7%. Seattle and San Francisco had double-digit decreases in house prices at -12.4% and -11.2%, respectively.

The April 2023 release of the Job Openings and Labor Turnover survey stated that job openings in the U.S. increased slightly to 10.1 million, with a job openings rate of 6.1%. Industries that saw the largest increase in job openings were retail trade; health care and social assistance; and transportation, warehousing, and utilities. Nationally, the number of hires remained relatively stable at 6.1 million, with a rate of 3.9%. Total separations in the nation decreased to 5.7 million, with a separation rate of 3.7%. The number and rate of quits remained unchanged, coming in at 3.8 million and 2.4 percent, respectively. On the other hand, the number of layoffs and discharges decreased to 1.6 million while the rate decreased to 1.0%. Other separations in the U.S. were little changed, reporting at 333,000.

The April U.S. trade deficit was $74.6 billion, up $14.0 billion from the revised $60.6 billion figure from March, seasonally adjusted. Exports decreased over the month 3.6% (or $9.2 billion) to land at $249 billion, while imports slightly increased 1.5% (or $4.8 billion) to $323.6 billion. While April saw an increase in the goods and services deficit, with the goods deficit increasing $14.5 billion to $96.1 billion and the services surplus increasing $0.6 billion to $21.6 billion, the year-to-date goods and services deficit has shown major shortening, decreasing $86.5 billion (23.9%) from the same period in 2022. Over the year, exports increased $55.9 billion (5.8%), and imports decreased $30.6 billion (2.3%).

Yuma managed to attain the largest non-seasonally adjusted year-over-year decrease in unemployment rate, dropping 2.0 percentage points to fall to 9.2%, according to the preliminary unemployment estimates by the U.S. Bureau of Labor Statistics. Yuma was also the only county in Arizona to experience a month-over-month increase in unemployment, ticking up 0.1 percentage points from 9.1% in March. Flagstaff had a slight decrease in unemployment over the month, shifting down 0.3 percentage points to 3.2%. The remaining Arizona metropolitan areas saw no change in unemployment rates, with Lake Havasu City-Kingman at 4.0%, Phoenix-Mesa-Scottsdale at 2.9%, Prescott at 3.2%, Sierra Vista-Douglas at 4.0%, and Tucson at 3.2%. The lowest unemployment rates in the nation were in Dover-Durham NH-ME and Manchester, NH at 1.1% each while El Centro, CA retained its rank of the highest unemployment rate among all U.S. metropolitan areas at 14.1%.

The U.S. unemployment rate rose to new heights for the year, ascending 0.3 percentage points to 3.7%, with the number of unemployed persons rising 440,000 to 6.1 million. The unemployment rate has ranged between 3.4% and 3.7% since March of 2022, so further increases in the unemployment rate could have consequences regarding consumer and business confidence in the economy. Despite the rise in unemployment, the number of people employed part time for economic reasons remained relatively constant at 3.7 million. Similarly, the labor force participation rate (62.6%), number of persons not in the labor force who want a job (5.5m), and the number of discouraged workers (422,000) were all essentially unchanged over the month. In May, job gains occurred in professional and business services (+64,000), government (+56,000), health care (+52,000), leisure and hospitality (+48,000), construction (25,000), transportation and warehousing (+24,000), and social assistance (+22,000). Other industries were largely unchanged. Average hourly earnings for all employees on private nonfarm payrolls edged up by 11 cents, or 0.3%. Additionally, with this release, total nonfarm employment for March (+52,000) and April (+41,000) were revised upwards, showing 93,000 more employment than previously reported.

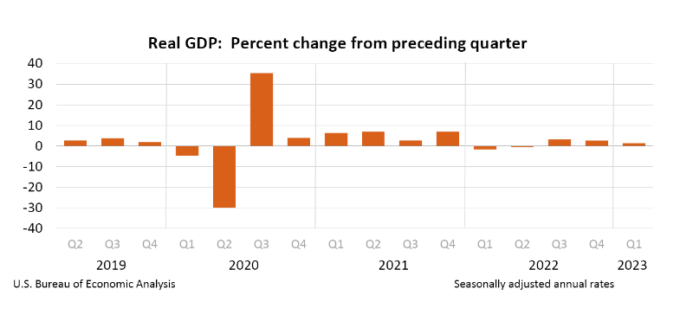

In the first quarter of 2023, secondary estimates provided slight upwards revisions for both real GDP and current-dollar GDP, with real GDP climbing 0.2 percentage points to 1.3% and current dollar GDP exceeding that growth with a 0.3 percentage point shift, ascending to 5.4%. On the other hand, the Bureau of Economic Analysis also released their first estimate for real gross domestic income (GDI), coming in at -2.3%. The average of real GDP and real GDI, a supplemental measure of economic activity, similarly turned out negative at -0.5%. Inflation indices all saw little to no change, with PCE price index excluding food and energy increasing 0.1 percentage points to 5.0% and the others remaining constant, with PCE price index at 4.2% and gross domestic purchases price index at 3.8%. This release also brought updates to fourth quarter 2022 wages and salaries, showing downwards revisions to wages and salaries (down $135.4b to $53b), personal current taxes (down $16.2b to $20.3b), and contributions for government social insurance (down $17.4b to $8.1b). With these revisions, real GDI is now estimated to have decreased 3.3% in 2022q4, a downwards revision of 2.2 percentage points.